Stablecoins are becoming a practical way for businesses to move dollars on the internet.

That sentence sounds simple. It is not.

For years, crypto sounded like a trading venue. Stablecoins change the frame. They turn blockchains into payment rails, treasury rails, and settlement rails. A business does not need to care about every token. It needs to know whether digital dollars can move safely, quickly, and with enough capacity to matter.

Solana is now one of the networks where that question has a serious answer.

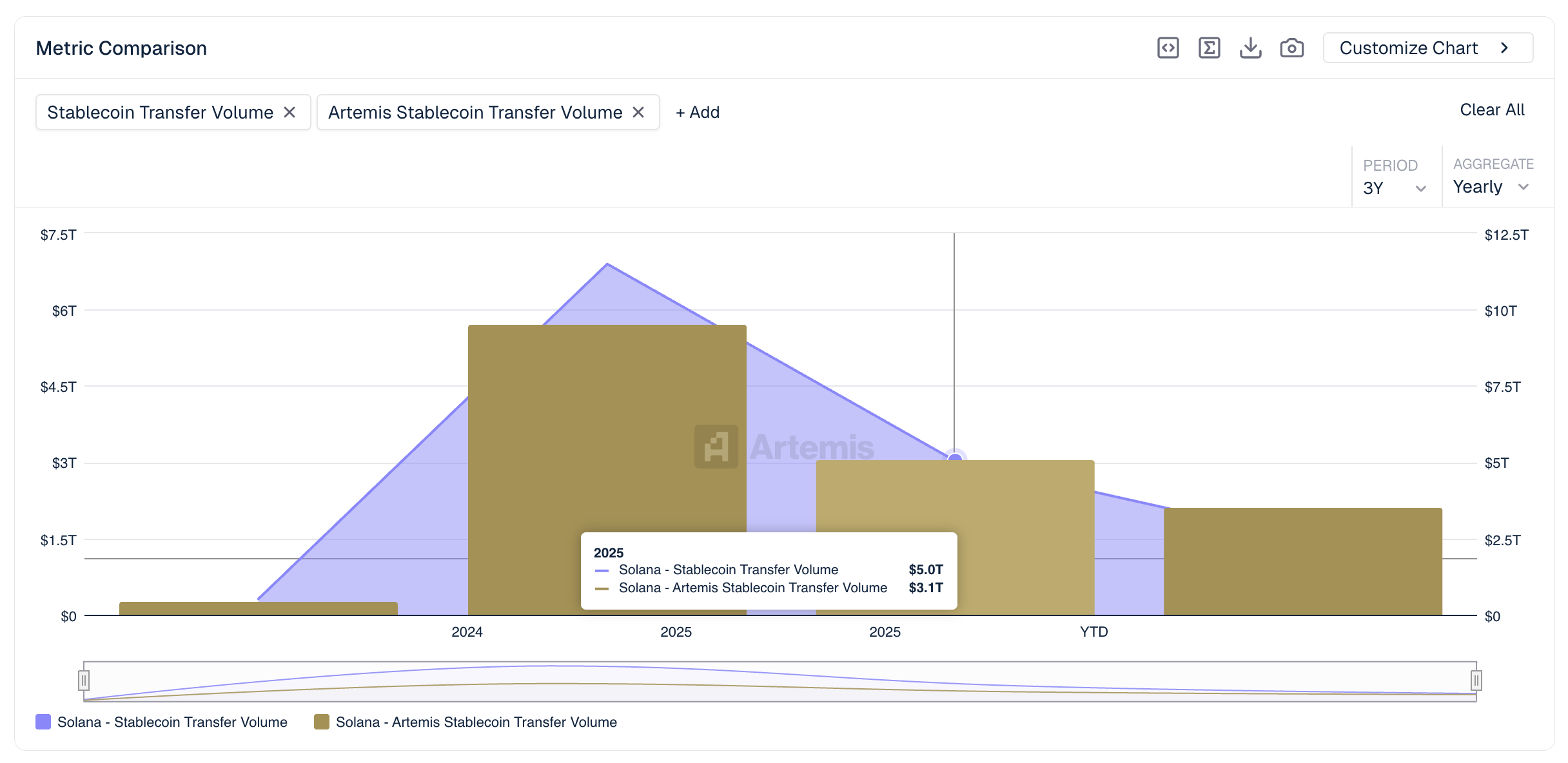

DeFiLlama shows roughly $15-16B of stablecoins circulating on Solana, making it one of the largest public networks for digital dollars after Ethereum and Tron. The stronger signal is usage: Blockworks reported that Solana stablecoin transfer volume reached $2.1T in Q1 2026, up roughly 60% quarter over quarter and year over year, excluding flash loans and other inorganic activity.

For a business, the point is not the ranking. The point is that there is already enough dollar movement on Solana for real workflows to exist: vendor payments, customer deposits, exchange settlement, treasury movement, and cross-border transfers.

The timing matters because regulation is also changing. The GENIUS Act became Public Law 119-27 on July 18, 2025, creating a federal framework for payment stablecoins in the United States.

That does not make every stablecoin product safe. It does make the category easier for enterprises to understand. Stablecoins are moving from ‘crypto thing’ to ‘regulated dollar instrument.’ That shift matters for compliance teams, finance teams, and founders selling to businesses that cannot afford regulatory ambiguity.

So the useful question is not ‘Are stablecoins real?’

The useful question is: ‘Is there enough usable dollar capacity on Solana for a business to start building?’

I think the answer is yes.

Market liquidity is the current observable state. In plain English, it asks: how much usable dollar capacity exists today?

Anticipated market liquidity is the forward-looking version. It asks: how much usable dollar capacity is likely to exist when a company ships, scales, or migrates more of its payment operations?

The distinction matters. A business does not adopt payment infrastructure for one transaction. It adopts infrastructure because it expects more volume, more counterparties, and more operational leverage over time.

The current business case is simple: Solana has about $15-16B of stablecoin supply, more than $2T of quarterly stablecoin transfer volume, and a growing set of dollar instruments beyond USDC and USDT, including PYUSD, USDG, USD1, and tokenized cash products.

The forward-looking case is more interesting. A conservative next-12-month range is roughly $18-25B of stablecoins on Solana. The more aggressive long-range case is that if the global stablecoin market grows toward $2T by 2028 and Solana keeps roughly its current 5% share, Solana stablecoin supply would be near $100B.

That is the enterprise argument.

A company adopting Solana stablecoin payments today is not just adding a crypto feature. It is preparing for a world where more invoices, payroll flows, vendor payments, cross-border transfers, and customer deposits can move over faster dollar settlement infrastructure.

There is one caveat: liquidity is not one number.

A market can have a lot of dollars in it and still be hard to use for a specific transaction. Venue matters. Counterparty matters. Compliance matters. The path from bank account to stablecoin wallet matters. The path back matters too.

That is why the transition should start with narrow workflows. Do not move the whole company treasury on day one. Start with one payment rail, one vendor corridor, one customer deposit flow, or one internal settlement use case. Measure cost, speed, failure rate, compliance overhead, and operational complexity.

Stablecoins will not replace banking all at once.

They will enter through the workflows where the old system is slowest.

Solana already has enough digital dollar liquidity to make those experiments worth running.